Key Takeaways

- Crypto cashback lets you earn cryptocurrency on everyday card purchases

- There are four card types: prepaid top-up, auto-convert debit, collateral-backed credit, and traditional credit with crypto rewards

- Crypto.com slashed rewards in 2022 and cut more perks in late 2025

- Stablecoin cashback (USDC, USDT) removes token volatility risk but some platforms cap monthly earnings at very low amounts

- Every crypto card purchase may trigger a taxable event in most jurisdictions

Crypto cashback cards have been around since 2018, but the landscape in 2026 looks very different from the era of generous CRO staking rewards and Spotify rebates. The promise remains the same: earn cryptocurrency simply by spending money you would have spent anyway. Whether that promise delivers depends heavily on which card you choose, which tier you hold, and how you account for fees, token price risk, and excluded merchant categories. According to Crypto.com’s annual Market Sizing Report released in February 2026, global cryptocurrency ownership reached 741 million in 2025 – yet many of those holders are still unaware of the gap between advertised and effective cashback rates on the cards they carry.

This guide explains how each type of crypto cashback card works, breaks down the real effective rates behind the headline numbers, reviews the major cards available globally in 2026, and covers what Reddit users have found through actual experience. It also addresses the tax and risk side of the equation that most card marketing materials quietly skip.

What Is Crypto Cashback and How Does It Work?

Crypto cashback is a rewards mechanism where a percentage of your card spending is returned to you in the form of cryptocurrency rather than traditional cash or points. The cryptocurrency is typically credited to your platform wallet or vault within 24-48 hours after a transaction settles, though some platforms batch payouts monthly.

The mechanism behind the scenes varies by card type. Understanding which model a card uses matters both for how your funds are handled and how each transaction is treated for tax purposes.

| Card Type | How It Works | Pros | Cons |

|---|---|---|---|

| Prepaid (top-up) | Load fiat/crypto first, then spend | Simple, budget control | Idle funds, top-up fees/spread |

| Debit (auto-convert) | Crypto sold at point of sale | Stay invested until purchase | Each spend = potential taxable event |

| Credit (collateral) | Borrow against staked crypto | No sale = no tax event, earn yield on collateral | Liquidation risk if collateral drops, interest rates |

| Credit (traditional) | Standard credit line, rewards in crypto | Consumer protections, no crypto needed | Credit check required, rewards in volatile tokens |

Most modern crypto cards in 2026 use the auto-convert debit model or the collateral-backed credit model. The auto-convert model is simpler: you hold crypto, the card sells it at the moment of purchase, and your cashback is credited in a designated token. The collateral-backed model, pioneered by platforms like ether.fi and Nexo, lets you borrow against your crypto without selling it – meaning your ETH or BTC keeps earning yield while you spend.

How to Get Started with Crypto Cashback

Crypto cashback requires no technical knowledge or complex strategy. The setup process is similar across most platforms and takes under 30 minutes from sign-up to first eligible purchase.

Step 1: Choose a Platform and Card

Select a card that fits your geography, spending habits, and appetite for complexity. If you want the simplest possible start with no staking and no token exposure, options like Gemini (US), Coinbase Card (US/EU/UK), or Bleap (global) require only an account and KYC. If you want higher rates and are comfortable holding a platform token, Crypto.com or Nexo offer tiered programs – but read the full terms before locking capital.

Step 2: Complete Identity Verification (KYC)

Every regulated crypto card requires KYC verification before cashback can be activated. You will typically need to submit a government-issued ID, a selfie, and confirm your phone number. Processing times range from instant to several days depending on the platform and your jurisdiction. Users in countries with non-standard address formats (parts of Latin America, Southeast Asia) have reported delays – account for this before expecting to use the card immediately.

Step 3: Fund Your Account or Link a Payment Method

After verification, add funds to your account. Options vary by platform: deposit crypto directly, transfer fiat via bank wire or SEPA, or link a bank account for recurring top-ups. For prepaid cards, you load a balance before spending. For auto-convert debit cards, funds stay in your crypto wallet until the moment of purchase. For collateral-backed credit cards like ether.fi or Nexo, you deposit crypto as collateral and the platform extends a spending limit against it – your crypto remains in your wallet earning yield.

Step 4: Make Eligible Purchases

Once funded, use the card at any Visa or Mastercard-accepting merchant online or in-store. Most platforms integrate with Apple Pay and Google Pay for contactless payments. Every eligible transaction triggers a cashback event. The crypto cashback percentage is applied to the transaction amount and typically credited to your account within 24-48 hours, or batched monthly on some platforms like ether.fi.

Step 5: Track and Manage Your Rewards

Monitor crypto cashback through the platform’s app or dashboard. Keep a record of reward amounts and their value at the time of receipt – this matters for tax reporting in most jurisdictions. Set up automatic exports from the platform’s transaction history to connect with a crypto tax tool like Koinly or CoinTracker.

What Purchases Do Not Qualify for Cashback?

This is one of the most misunderstood aspects of crypto cashback cards. Most platforms exclude a significant number of transaction types from earning rewards. Common exclusions across major platforms include:

- ATM withdrawals – universally excluded across all major cards

- Utility bill payments and rent in many jurisdictions

- Peer-to-peer transfers (PayPal, Venmo, bank wire)

- Money orders and cash advances

- Government services and tax payments

- Gambling and gaming transactions

- Certain merchant category codes (MCCs) at the platform’s sole discretion – and these can change without prior notice

One Reddit commenter put it plainly: ‘there is no cashback for ATM withdrawals, that would be a money glitch.’ A user with years of CDC experience noted: ‘some merchant codes have always been exempt – this is why paying bills or cash advance doesn’t generate cashback.’ The exclusion lists are real, often buried in help articles, and they can change. One ether.fi user reported being banned from the platform’s Discord after asking why certain MCC 5734 merchants received cashback while others in the same category were excluded with no explanation provided.

The Headline vs Effective Rate Problem

Perhaps the most important thing to understand about crypto cashback: the rate you see advertised is almost never the rate you actually receive. The gap between headline and effective rates is driven by four main factors.

Conversion Spreads and Top-Up Fees

Many prepaid crypto cards add a spread when you convert crypto to load the card balance. One Reddit user described this with Crypto.com: ‘when you load up the card with BTC, they will decrease the value of BTC by some percentage – instead of $85,000 BTC, they will say it is $84,000.’ This spread is effectively a hidden fee that directly reduces your net crypto cashback. On a 2% cashback card with a 1% top-up spread, your effective return on spend is closer to1% before any other factors.

Monthly Earning Caps

Many cards impose hard caps on crypto cashback earnings per month. Crypto.com’s Ruby Steel caps rewards at $25 per month – meaning a user spending $5,000 monthly effectively earns just 0.5% back, not 2%. The Jade and Royal Indigo tiers are capped at $75 per month. Only higher tiers with significant CRO staking requirements remove the cap.

One community member noted that Nexo quietly changed terms in late 2025: ‘You quietly changed the terms and capped all cashback – across every tier including Platinum – at just $10 per month. I’ve loved Nexo for years but you’ve just lost a long-time customer.’ Nexo later clarified this was a temporary campaign cap rather than a permanent change, but the confusion illustrates how quickly reward structures can shift.

FX Fees on Non-Local Currency Spending

Foreign transaction fees (FX fees) can significantly erode cashback value for international users. Crypto.com charges 0.5% to 1.5% FX fees on lower tiers, though EU/UK higher-tier users gained 0% FX fees as part of the September 2025 Level Up update. The ether.fi card charges 1% on non-USD transactions. One Reddit user in Romania reported: ‘currency conversion from RON to EUR to top up the card, then back to RON when spending, meant my 3% cashback turned into about 1.5%.’ This is a common real-world experience that marketing materials rarely acknowledge.

Token Volatility

When cashback is paid in a platform’s native token (CRO, NEXO, PLU), the value you actually receive depends on the token’s market price at the time you redeem or sell it. Reddit is full of accounts of users who accumulated CRO cashback during 2021-2022 only to see its value fall over 80% from peak prices. As one user summarized: ‘if you directly convert your CRO to dollars, then yes, the cashback is real. Otherwise, all depends on the CRO price.’ Cards that pay cashback in BTC, ETH, or stablecoins (USDC, USDT) carry meaningfully less of this risk, though volatile assets still fluctuate.

| Card | Headline Rate | Effective Rate (typical) | Main Rate Killers |

|---|---|---|---|

| Crypto.com Ruby | 2% | ~0.7% net | 1% top-up spread, $25/mo cap |

| Bybit Card | Up to 10% | 2% – 4% | Caps, BNB holding req., FX fees |

| Plutus Card | 3% | 0.75% – 1.5% | Subscription fee (£14.99/mo), PLU cap |

| ether.fi Cash | 3% | ~3% (in wETH) | 1% FX on non-USD, borrow mode risk |

| Gemini Credit Card | Up to 4% | ~3% (dining), 1% other | Category caps, US only |

| Bleap Mastercard | 2% | ~2% (USDC) | Low monthly earning cap |

| Nexo (credit mode) | Up to 2% | 0.5% – 2% | Loyalty tier dependent, EEA/UK only |

Major Crypto Cashback Cards in 2026: An Honest Review

Crypto.com Visa Card

Crypto.com remains the world’s largest crypto card program, available in over 179 countries with more than 100 million registered users as of late 2025. Its tiered card structure runs from the free Midnight Blue (0% cashback) through Ruby Steel ($500 CRO stake, 2%), Royal Indigo and Jade Green ($5,000 stake, 3%), Frosted Rose Gold and Icy White ($50,000 stake, 4-5%), up to the new Obsidian ($400,000+ stake, 5%) and Prime tiers (8%). In September 2025 the platform launched Level Up, a unified subscription-or-staking program that also allows users to access card benefits via a monthly subscription starting at $4.99/month instead of staking CRO.

The honest history: In May 2022, Crypto.com slashed cashback rates across all tiers – in some cases from 8% down to 2% – and introduced monthly caps where none existed. CRO dropped 11% on the day of the announcement. In October-November 2025, the platform removed Amazon Prime, Expedia, Airbnb, and X Premium rebates for legacy cardholders. A community member with years of experience documented the pattern: ‘They have manipulated their rewards in multiple cycles now. CDC creates a coin, offers huge rewards for buying and locking up their funds, then cuts rewards in several stages once enough people have signed up with funds locked.’

What users genuinely value: Several long-term users report positive experiences when they entered at the right tier and price. One user who built their position from the base card upward shared: ‘Just finished our taxes, $12,000 in total rewards.’ Another noted: ‘the best time to get the card is when CRO is at its lowest – you get more CRO for the same spend.’ Gas cashback was frequently praised: ‘you get cashback buying gas; it adds up quickly if you drive a lot.’

Key restrictions to know: Utility payments, rent, and government services do not earn cashback. The 12-month CRO staking requirement means you cannot quickly exit if terms change. The top-up spread adds an effective cost of roughly 0.5-1% per purchase on lower tiers.

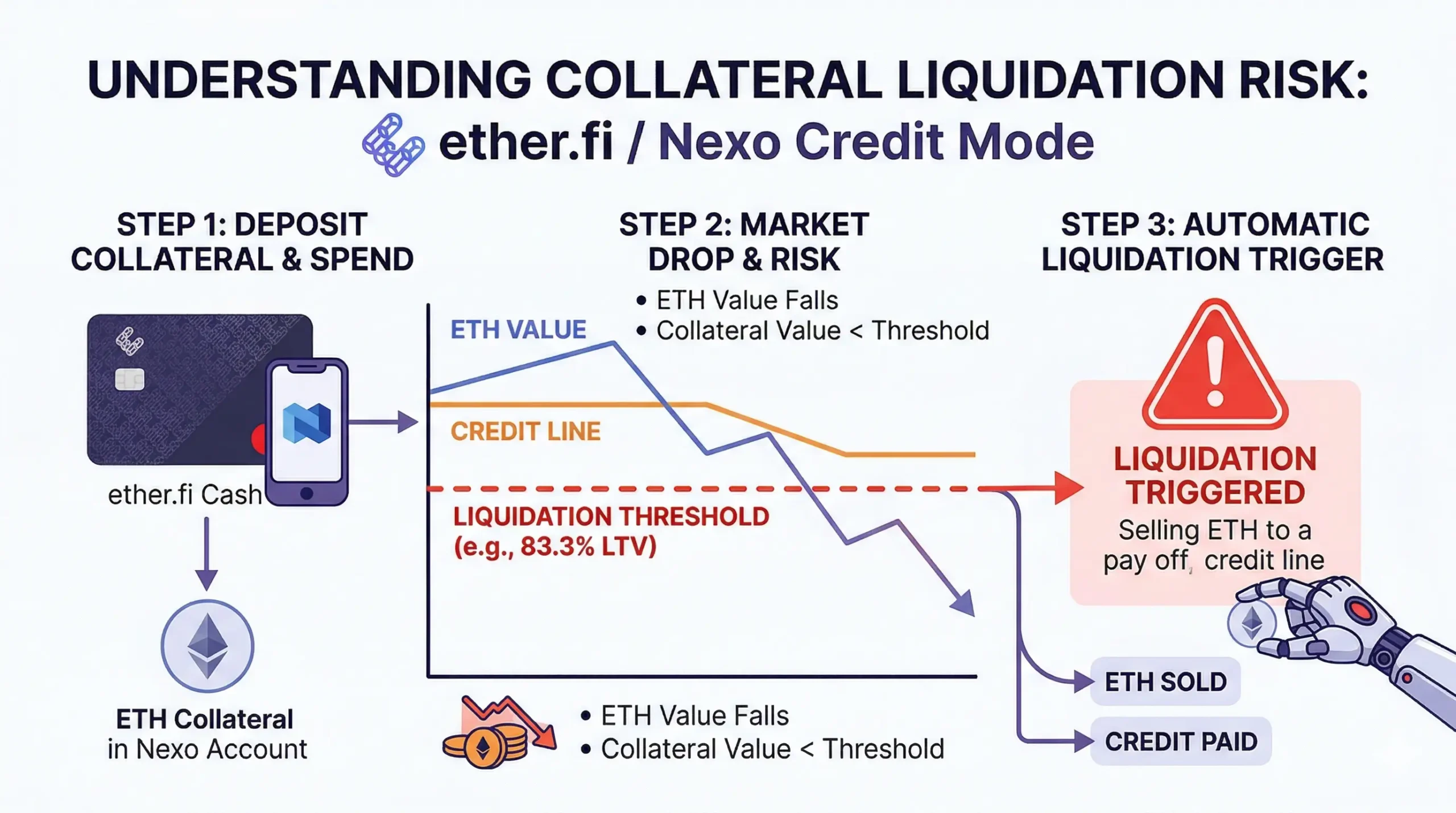

ether.fi Cash Card

ether.fi Cash is a DeFi-native Visa Signature credit card that launched in 2025 and has rapidly attracted attention for its non-custodial design. The core differentiator is its Borrow Mode: you deposit ETH as collateral into a Gnosis Safe vault, ether.fi borrows USDC against that collateral, and the USDC pays the merchant. Your ETH never moves and continues to earn staking yield through eETH – which one user described as ‘a 4% APY on the collateral, 5%+ APY on USDC in the vault, and 3% cashback on every purchase, all stacking simultaneously.’

Cashback rates: Standard tiers pay 2% (Core) and 3% (Luxe/Pinnacle) in wETH, credited monthly. As of early 2026, a promotional campaign has set all tiers to 3%. The card carries zero annual fee, no monthly minimums, and no cashback cap. Visa Signature protections are included across all tiers.

Community reception has been mostly positive for DeFi users, with one Latin American user describing it as ‘totally a game changer – I can use my crypto as collateral and earn rewards both on staking and cashback.’ A Reddit user in the UK thread: ‘upgraded from Wirex to EtherFi’ – framing it as a quality upgrade. However, Trustpilot reviews reveal real pain points: one user reported being banned from the Discord server after asking why two merchants in the same MCC category received different cashback treatment with no documented reason. Another reported months of KYC limbo for users in Latin America where address formats differ from the system’s expectations.

Key risk: Borrow Mode carries liquidation risk. If ETH’s price falls far enough, your collateral ratio may breach the liquidation threshold and your assets can be partially liquidated automatically. Users who prefer to avoid this risk can use Direct Pay Mode, which works more like a debit card drawing from stablecoins in the vault – but without the simultaneous yield earning benefit. The 1% FX fee on non-USD transactions is also a real drawback for international users.

Nexo Card

The Nexo Card is a hybrid debit/credit Visa card available across the European Economic Area and UK. Its dual-mode structure is genuinely unique:Credit Mode lets you borrow against your crypto holdings to make purchases (earning up to 2% cashback in NEXO tokens or 0.5% in BTC), whileDebit Mode pays no cashback but earns daily compound interest of up to 14% on your balance in NEXO tokens. Nexo has historically been one of the more reliable platforms for consistent payouts, with one user on Reddit reporting: ‘I am platinum tier and I’ve already gone beyond the usual $200 cashback limit this month.’

The card is not yet available in the US, though Nexo has confirmed it is working toward a US return. The UK lacks cashback entirely on the Nexo card, a recurring complaint in community threads: ‘Bring the cashback back to the UK already – Crypto.com does cashback here.’ Borrowing rates start at 2.9% APR in credit mode, rising to 18.9% for lower loyalty tiers – these costs must be factored against the cashback value for any spending done on credit. Holiday campaigns have offered boosted rates up to 10% cashback with spending multipliers.

Gemini Credit Card

The Gemini Credit Card is a US-only World Elite Mastercard issued by WebBank with no annual fee and no foreign transaction fees. It earns up to 3% back on dining, 2% on groceries, and 1% on all other purchases – instantly deposited in the cryptocurrency of your choice from Gemini’s supported assets. According to CryptoSlate’s April 2026 review, Gemini ranks first among US crypto cashback cards because its reward terms are clear before approval and easy to judge from day one. There are no staking requirements and no complex tier systems. The card requires a standard credit check, which distinguishes it from most crypto debit cards that skip credit underwriting.

Coinbase Card

The Coinbase Card is a Visa debit card available in the US, EU/EEA, and UK (restored in 2025). It earns 4% back in XLM or GRT, or 1% back in BTC or ETH with no annual fee and no staking requirement. The card auto-converts crypto from your Coinbase account at the point of sale – spending USDC carries zero conversion fees, making it effectively a free spending mechanism for stablecoin holders.

One user tested this by running a $17,000 car loan payment through the card and collecting $680 in crypto cashback before Coinbase flagged the account for terms of service review. A Coinbase One Card credit product was also announced for Fall 2025, requiring a Coinbase One membership ($4.99/month or $49.99/year) and offering 4% back in BTC with a $200,000 minimum balance requirement for the top rate.

Bybit Card

Bybit Card advertises up to 10% cashback but independent reviewers consistently note that effective rates land closer to 2-4% for most users after accounting for BNB holding requirements, monthly caps, and the 0.9% crypto conversion fee. The card is available across the EEA (excluding Croatia and Ireland) but not in the US or Australia. It earned MiCA regulatory compliance in the EU, which The Block noted as a significant trust factor. Free ATM withdrawals are limited to €100 per month, with 2% charged after that.

Shakepay (Canada)

For Canadian users, Shakepay is the primary Bitcoin cashback option. It offers a 3% crypto cashback promo rate in Bitcoin (Satoshis) on the prepaid Visa, dropping to 1% after a spending threshold. One Shakepay user reported accumulating 120,000 Sats since December and highlighted the ‘Round Up’ feature for additional accumulation.

The daily shake feature (a streak-based bonus) can boost effective rates significantly – one user reported an average of 7% when accounting for shake bonuses built up during the bear market. However, this is not a credit card (it is prepaid), carries no insurance like a credit card would, and charges FX fees. As one commenter noted: ‘You are further ahead using a high percentage fiat cashback credit card and DCA-ing separately into BTC.’ Both approaches are valid depending on your preference.

Bleap Mastercard and Other No-Fee Options

Bleap Mastercard offers 2% crypto cashback in USDC with no annual fee, no FX fee, no top-up fee, and no conversion fee – making it the cleanest fee structure in the market. The non-custodial MPC wallet design keeps assets in user control until payment. The main drawback is a low monthly crypto cashback cap that limits earning potential for higher spenders. Trustee Plus was mentioned by several community members as another low-friction alternative with a simple Visa setup and minimal requirements, though without flashy reward percentages.

Check out also our guide on Learn and Earn Crypto Programs: Get Free Crypto in 2026

Crypto Shopping Portals: Cashback Without a Crypto Card

Not all crypto cashback requires a dedicated crypto card. A separate category of platforms lets users earn cryptocurrency simply by shopping through partner retailers via apps, browser extensions, or dedicated websites. These portals work more like traditional cashback sites – no staking, no token lockup, no card application required.

Lolli is one of the most established examples, offering Bitcoin and cash rewards at over 25,000 partnered merchants through its browser extension and mobile app. Users can earn up to 30% back in BTC or cash at select retailers, though typical rates at mainstream stores sit between 1% and 6%. StormX operates similarly, allowing users to earn crypto rewards at a broad range of online retailers with rates that can occasionally reach double digits during promotional campaigns.

The key advantages of shopping portals over crypto cards:

- No staking requirement and no capital at risk

- No card application or credit check

- Works alongside any existing payment method – including traditional cashback cards

- Lower barrier to entry for users new to crypto

The trade-offs: Shopping portals only earn cashback at partner merchants – your grocery store or local restaurant is unlikely to be included. Rates are often promotional and can disappear. You are also dependent on the portal tracking your purchase correctly through affiliate links, which occasionally fails. For everyday spending across all categories, a crypto cashback card is more consistent. Shopping portals work best as a complement to a card strategy, not a replacement for one – stacking portal cashback with card cashback on the same purchase where supported.

Crypto Cashback vs Traditional Cashback: Is It Worth It?

A recurring community debate is whether crypto cashback cards actually beat the best traditional alternatives. One Reddit commenter offered a blunt comparison: ‘If you are American and you are not getting 3% back or more on credit card transactions, you are a sucker. The entire industry exists to funnel money from poor people to people who understand credit card rewards.’ Another noted: ‘For a $50 annual fee I would rather go with the Robinhood Gold card – more reliable cashback and the other features more than offset the annual fee.’

The honest comparison: Traditional premium cashback credit cards (Chase Sapphire, Amex, Citi) typically offer 1.5-3% back in fiat with signup bonuses worth $600-$1,500 and strong consumer protections (chargebacks, purchase protection, travel insurance). Crypto cashback cards can match or exceed these rates but introduce several variables traditional cards do not:

- Reward token volatility – your 2% cashback in CRO may be worth 0.5% if the token drops 75%

- Platform risk – if the issuer fails (as Celsius and BlockFi did), rewards and balances may be lost

- Fewer consumer protections – most crypto debit cards lack the chargeback rights and fraud protections of traditional credit cards

- Tax complexity – every conversion and cashback receipt may be a reportable event

The strongest argument for crypto cashback cards: if you are already holding crypto and believe in its long-term value, earning crypto rewards in BTC, ETH, or stablecoins is a form of passive dollar-cost averaging. One community member described holding XYO cashback through a full market cycle and accumulating the equivalent of $200-300 over a year purely from passive card use. Another user who entered early: ‘my base amount for the card is around 120% up as of today if I wanted to sell.’ The upside exists – but it is not guaranteed and it requires patience through volatility.

How to Read a Crypto Cashback Card’s Real Value

Before applying for any crypto cashback card, run this calculation:

- Estimate your monthly spend: and identify which categories are actually eligible (exclude bills, utilities, P2P, ATM)

- Find the effective rate: subtract top-up spread (0-1.5%) and FX fees from the headline cashback rate

- Apply the monthly cap: divide the cap by your eligible spend to find the true rate at your spending level

- Value the reward token: cashback in USDC or BTC is worth more than cashback in a platform’s native token that may not have a liquid market or may lose value

- Factor in staking cost: if you need to lock $5,000 in CRO for a year to get 3% back, calculate your opportunity cost against what you would earn in yield or appreciation with that capital elsewhere

- Read the full exclusion list: find the current help article on merchant category restrictions and confirm your primary spending categories qualify

What to Do with Your Crypto Cashback Rewards

Cashback tokens are not income – they are bonus crypto. What you do with them shapes whether cashback becomes meaningful over time or simply noise in your wallet.

Hold the tokens

If you receive cashback in BTC, ETH, or a stablecoin you believe in, holding is the simplest approach. This turns every purchase into a micro-investment, effectively dollar-cost averaging into your preferred asset passively through spending. Several Reddit users described this as their primary cashback strategy: ‘it’s like automatic passive DCA – when the price is low you get more CRO, so you want CRO to be low while you are purchasing.’

Convert to a preferred asset

If your crypto cashback is paid in a platform’s native token (CRO, NEXO, PLU) and you do not want exposure to it, the most common approach is to convert it immediately into BTC, ETH, or a stablecoin on the same platform. This avoids the volatility risk of holding a single-platform token while still capturing the cashback value. Be aware that conversion may trigger a taxable event in most jurisdictions.

Stake the rewards for additional yield

Some platforms allow you to deposit cashback directly into a staking or earn product. One Shakepay user described stacking card cashback with Gemini Earn for an additional yield layer on top. On platforms like Nexo and Crypto.com, earned crypto cashback in the native token can often be restaked to boost loyalty tier benefits – though this deepens your exposure to the platform token.

Cash out periodically

For users who want zero ongoing crypto exposure, most platforms allow conversion to fiat and withdrawal to a bank account. This is the simplest approach but removes the upside potential of holding. It also crystallizes any taxable gain or income at the time of sale. If your cashback token has appreciated since receipt, you will owe capital gains tax on the difference in addition to any income tax already owed on receipt.

Risks and Downsides of Crypto Cashback Cards

Platform Risk and Benefit Cuts

The crypto card space has a documented history of platforms unilaterally reducing benefits after users have locked in capital. Crypto.com’s 2022 reward cuts and 2025 benefit removals are the clearest example, but the pattern is not unique. As one long-time community member explained: ‘they can reduce the cashback at any given time, and they can set a monthly limit once things go sour. It has happened in the past, and it will in the future.’ Locking $50,000 in CRO for 12 months provides no contractual guarantee that the cashback rate will remain the same for that period.

Token Concentration Risk

Platforms that reward you in their own native token create a compounding exposure. You lock capital in the token to get card access, and you earn more of the same token as cashback. If the platform struggles, both your staked capital and your earned rewards lose value simultaneously. This is the core criticism raised repeatedly in community threads: ‘The thing is the rewards are based on a shitcoin they create from thin air.’ Choosing cards that reward in BTC, ETH, or stablecoins avoids this concentration.

Collateral Liquidation Risk

For DeFi credit cards like ether.fi Cash in Borrow Mode, liquidation is a real and automatic risk. If your ETH collateral drops below the platform’s maintenance margin (typically 80-85% loan-to-value), the system automatically sells collateral to bring the ratio back in line. During volatile market conditions, users can lose a portion of their holdings without any manual action on their part. This risk is manageable by maintaining conservative collateral ratios and monitoring positions regularly, but it is not present with traditional cards or simple debit cards.

Tax Implications of Crypto Cashback in 2026

This section applies globally and the rules are tightening significantly in 2026.

The United States

The IRS treats crypto cashback differently depending on card type: credit card rewards (when earned on a traditional credit line) are generally considered non-taxable rebates. However, debit card cashback paid in cryptocurrency is typically treated as ordinary income at the fair market value of the tokens at the time of receipt.

Additionally, each time a crypto debit card converts assets to fiat at the point of sale, that conversion is a taxable disposal event – triggering capital gains or losses based on the difference between your cost basis and the current price. Users spending BTC they bought at $20,000 when BTC is at $90,000 realize a taxable gain on every single purchase. Spending USDC avoids this issue since there is typically no gain to realize on a stablecoin.

Starting with the 2025 tax year, Form 1099-DA requires custodial brokers to report gross proceeds from crypto transactions. From 2026 onwards, cost basis reporting is also required. This significantly increases the paper trail available to the IRS for crypto card spending.

United Kingdom

HMRC treats crypto cashback from debit cards asmiscellaneous income in most cases, taxable at income tax rates (20-45%). Each crypto-to-fiat conversion at point of sale can trigger a capital gains event. From January 2026, the Cryptoasset Reporting Framework (CARF) requires UK-based crypto platforms to automatically report all user transactions to HMRC, including crypto debit card payments. The Treasury estimates this framework will recover £315 million in unpaid tax by 2030.

European Union

The EU’sDAC8 directive entered operational implementation from January 1, 2026, requiring crypto service providers to collect and automatically report user transaction data to national tax authorities. Rules differ by member state – Germany holds crypto tax-free after one year of holding, France applies a 30% flat rate on gains, Italy taxes gains above €2,000 per year at 26%. EU users should review their specific country’s rules.

Canada, Australia, and Other Markets

Canada treats crypto gains as capital gains or business income depending on frequency of trading. The 50% capital gains inclusion rate applies to most individual investors. Australia treats crypto as property subject to capital gains tax, with a 50% discount for assets held over 12 months. Both countries are implementing CARF-aligned reporting frameworks that will give tax authorities access to exchange transaction data.

The practical takeaway: crypto card spending is not tax-free anywhere in the developed world. Users who have not been tracking their card transactions and cost basis should consult a qualified crypto tax professional before the next filing deadline. Automated tools like Koinly, CoinTracker, or Coinbase’s built-in tax reports can significantly simplify record-keeping.

How to Choose the Right Crypto Cashback Card

The right card depends on your geography, existing crypto holdings, spending volume, and tolerance for complexity.

- US users wanting simplest setup: Gemini Credit Card – clear rates, no staking, no annual fee, instant crypto deposits. Requires a credit check.

- US/Global users with significant ETH holdings: ether.fi Cash – earn staking yield on collateral simultaneously with crypto cashback. Understand Borrow Mode liquidation risk before using it.

- EU users: Bybit Card (MiCA compliant) or Nexo Card (for ETH holders who want credit mode). Compare your spend level against each card’s caps before committing.

- Users who want stable, volatile-free cashback: Cards paying in USDC (Bleap, COCA) remove token price risk entirely. Bleap’s monthly cap limits high-spender value.

- Canadians: Shakepay provides the most accessible BTC cashback option. Compare the effective rate honestly against a high-percentage fiat cashback credit card plus manual BTC purchases.

- Heavy spenders on Crypto.com’s ecosystem: Level Up subscription may outperform CRO staking on a risk-adjusted basis. Calculate the math honestly: staking $5,000 in CRO for 3% crypto cashback may not beat the $4.99/month subscription if you spend over $2,000/month.

Frequently Asked Questions

Not exactly. You are exchanging something: either spread on top-ups, the opportunity cost of locked staking capital, the risk of holding a volatile reward token, or in the case of DeFi credit cards, the liquidation risk on your collateral. Crypto cashback is a real benefit when the reward exceeds these costs – but for many lower-tier users, the net gain is smaller than the headline rate suggests.

Yes. Several cards require no staking: Gemini Credit Card, Coinbase Card, ether.fi Cash (Core tier, no mandatory staking), Bleap Mastercard, and Shakepay all offer crypto rewards with no mandatory token purchase. Gemini and Coinbase require US residency. Bleap and ether.fi are available more broadly.

This depends on the custody model. If your cashback is held in a custodial platform wallet (Crypto.com, Bybit, Nexo), it may be at risk in a platform insolvency – as Celsius and BlockFi demonstrated. If cashback is deposited to your own non-custodial wallet or a regulated brokerage account (Gemini, Coinbase), the risk is lower but not zero. The safest practice is to regularly withdraw earned rewards to a wallet you control.

In most countries, yes. Each time a debit card converts crypto to fiat at the point of sale, that is a taxable disposal event in the US, UK, EU, Canada, and Australia. The gain or loss depends on your cost basis in the crypto. Spending stablecoins typically avoids this because there is no gain to realize. Collateral-backed credit cards (ether.fi, Nexo credit mode) may avoid the disposal event since you are borrowing rather than selling.

No, and this is a key risk. Platforms can change merchant category exclusions at any time, often without advance notice. The Crypto.com community has documented multiple instances of categories being quietly added to the exclusion list post-card issuance. Always check the current exclusion list on the platform’s help center before relying on cashback from a specific category.

It depends on your timeline, risk tolerance, and entry price. Users who entered when CRO was at low prices and held through a bull run have reported strong returns. Users who entered near the peak in 2021 saw their staked capital and cashback both decline over 80%. The current Level Up subscription model ($4.99/month for the Plus tier) offers an alternative that avoids token price exposure – whether it is better value depends on your monthly spend level.

For zero or low FX fees globally: Crypto.com Jade+ (0% FX in EU/UK on September 2025 update), Coinbase Card (no added FX fee), ether.fi Cash (1% FX – modest), Wirex (0% on certain tiers). Always confirm current terms for your region, as FX fee structures are frequently updated.